by Viktoriya Khusit | Nov 11, 2017 | Blog |

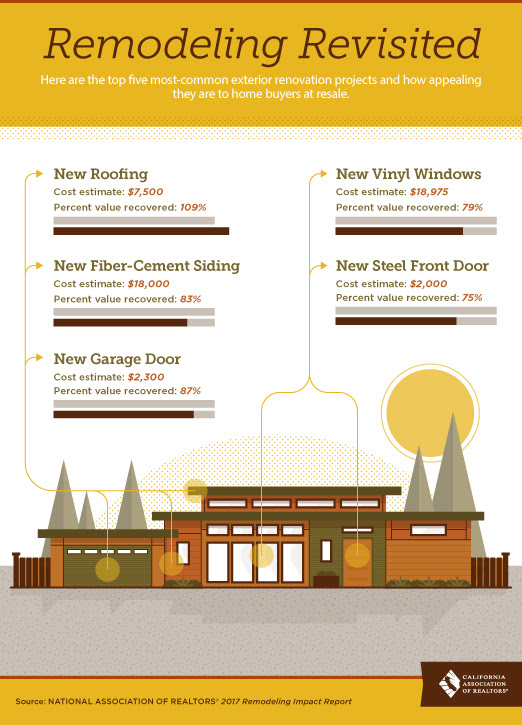

While working on a blog article regarding home improvements that pay, I came across this post on the www.CAR.org (California Association of Realtors), and simply could not not to share. While remodeling does not really increase your selling price, it definitely improves chances of selling faster if house priced at the market average level. However, here is 5 exterior renovation projects that will recover or almost recover money put in into them.

by Viktoriya Khusit | Oct 26, 2017 | Blog |

While working on real estate investment properties deals, I get a lot questions like “what is my taxes will be when I sell my investment property, is it true tax is 39%?”

Short answer is “NO”, longer answer is “anywhere between 0% and 25%.”

Every asset (example an investment property) has a basis. Basis is the amount taxpayer has invested into an asset. Cost basic is the purchase price plus commissions plus costs incurred to make the purchase. Adjusted basic is cost basic plus or minus adjustments. Fox example amount spent on a new roof will be added to cost basic, but depreciation claimed in the previous years will be subtracted from the cost basis.

Depending on the nature of the assets, gains can be taxed at the different rates. Most properties that taxpayer uses for personal or investment (primary residence, household furnishings, stocks or bonds, personal auto, jewelry, coins and stamp collections) use are capital assets. However, anything that used in a business -land, buildings, equipment and inventory often referred as “capital assets” by public, are noncapital assets. Real property and depreciable property used in a trade or business are not capital assets. So “Investment property” which is used to produce rental income is not considered a capital asset.

Holding period: Short term-less than a year. Long term-more than 1 one year.

Sales price-adjusted basis= gain or loss

Sales price= amount realized from sale-any direct selling expenses such a commissions or brokerage fees.

To encourage and reward long-term capital investment, the federal government taxes capital gains at a lower rate than ordinary income.

Short term (less than a year) capital gains are taxes at the same rate as ordinary income. Assets that are held more than 365 days (long term) are taxed at 0%, 15% and 20%

Knowing all these information, let’s go back to original scenario, of selling a rental property.

Per IRS, Rental property is not a capital asset, it’s a noncapital asset, and would result in ordinary income tax rates; however, IRS section 1231 allows certain business assets to be treated as if they were capital assets. There are some steps involved in qualification of the business assets into IRS sections 1231, and then into 1245 and 1250, (which will not be discussed here) but in short taxpayer is required to calculate the “unrecaptured Section 1250 gain”- which is amount of the depreciation taken on the property that is not recaptured as ordinary income under Section 1250 and taxed at 25% and the remaining capital gain will be taxed at appropriate regular capital gains rate of 0, 15 or 20%.

As an example: Mr. Smith bought investment property 5 years ago for $478,000. Depreciation taken on this property over the years was $168,000. He sales his property for $756,000. Gain of the sale is $446,000. $168,000 (depreciation) will be taxed at 25%, and remaining $446,000-$168,000=$278,000 is taxed at 20%.

Hope you enjoyed reading this and call us if you have any tax or real estate needs or questions.

by Viktoriya Khusit | May 22, 2017 | Blog |

A Federal Tax Lien is a claim against property. When you don’t pay your fist tax due a lean is filled and it is attached to any property you owe or any future rights you may have to a property. This lien is reported to credit reporting agencies and have negative effect on your credit rating and make difficult for you to receive a credit such a loan or a credit card. Once your debt is fully paid off, Federal Tax Lien gets “released” or it can be “withdraw” if you make arrangements with IRS such as installment Agreement.

Levy is a seizure of property. While a Lien is claim against your property, Levy is actual legal seizure where IRS actually takes your property or a right to a property to satisfy your tax debt. If you have current Installment agreement or Offer in Compromise, IRS cannot asses a levy.

Example of property that can be “levy”:

-Wages, salary or commission, bank accounts, federal payments, house, car or other property

Property that cannot be seized:

-Unemployment benefits, certain pension benefits, workers compensation, certain public assistance payments, minimum weekly exempt income, court ordered child support

by Viktoriya Khusit | May 9, 2017 | Blog |

Now tax season is over and hopefully you filled your tax return. In my practice I have a few clients who owe a balance due on their returns. My first and main advise- FILE. File your returns regardless of you having funds to pay your balance due. If you don’t file before a due date, you will be automatically assessed a fee for ” failure to file your tax return”. You filled on time-you already saved money.

So you have a balance, what is your options of paying it.

Best option is to pay it in full before a due date or after if you have to. This can be done via direct debit ( and IRS will take only amount you indicated on the date you indicated on your authorization. Second option is a payment via credit/debit card. You can do it by go to https://www.irs.gov/uac/pay-taxes-by-credit-or-debit-card

Third option you can mail a physical check to the IRS.

What if you need time or help to pay your balance. There are two options available:

Installment Agreement and Offer of Compromise

Installment Agreement is a contract with IRS, where IRS allows to make smaller periodic payments over time. You can apply online https://www.irs.gov/individuals/online-payment-agreement-application

or over the phone 1-800-829-1040

or by mail. If your balance is less than $25,000 you need form 9465 if more than $25,000, use form 9465-FS . Also you can fill out form 2159 Payroll Deduction agreement.

and of course in person.

Remember you will still be charged applicable penalties and interest. Also, a Notice of Federal Tax Lien can be filled against you, and this lien goes on your credit until you pay your balance in full, but IRS will send you a letter warning you that they are planning on filling a lien.

Offer in Compromise may be accepted by IRS if you cannot pay in full or even through installments. In short, you will ask IRS to settle unpaid taxes for less than what you owe. Offer in Compromise may be accepted if:

– IRS agrees that tax debt amount may not be accurate,

-Taxpayer has insufficient assets and income to pay balance due

– or you have exceptional circumstances and paying a balance due would course an economic hardship or would be unjust

Form 656-L needs to be filled out if tax debt inaccurate or form 656 if a taxpayer unable to pay due to hardship